49 Item Checklist to Reduce Chargebacks

What are chargebacks, what is a bad chargeback ratio, reasons chargebacks occur, how to mitigate each and more.

7/7/202511 min read

What is a chargeback?

A chargeback is when money from a completed credit or debit card transaction is reversed and returned to the cardholder, usually because they disputed the charge with their bank.

Why is it important to manage your chargebacks as a merchant?

1. Financial Impact

Every chargeback usually means lost revenue (the original sale amount).

You pay chargeback fees (often $20–$100 per case).

Even if you win the dispute, the process costs time and resources.

2. Risk of Losing Payment Processing

Your payment provider and card networks (Visa, Mastercard, etc.) monitor chargeback rates.

Too many chargebacks can land you in a high-risk program with stricter rules and higher costs.

In extreme cases, your payment processor may terminate your account, cutting off your ability to accept cards.

3. Improved Customer Satisfaction and Operational Efficiency

A high number of disputes may signal poor service, miscommunication, misleading product descriptions, fulfillment issues or fraud prevention gaps. By managing them, you can identify problems early and fix them, which makes customers happier and streamlines operations.

What Chargeback ratio should my business have?

There are 3 key metrics to measure (specific to Visa transactions):

Reported Fraud: The transaction was reported as fraud by the cardholder’s bank (often called TC40 ratio)

Reported Chargebacks: Official dispute, money is reversed unless merchant successfully contests (often called TC15 ratio)

All Settled Transactions (often called TC05 ratio)

Note:

When Reported Fraud cases become a Reported Chargeback, these cases are counted separately and not combined like previously

Includes all card not present transactions globally (transactions not made in person i.e. online)

Excludes Reported Chargebacks (TC15) resolved with RDR or Compelling Evidence 3.0.

To calculate your chargeback ratio:

Reported Fraud + Reported Chargebacks

Divided by All Settled Transactions for the Calendar Month

Example:

Reported Fraud = 100 cases

Reported Chargebacks = 50 cases

All Settled Transactions = 10,000

Reported Fraud + Reported Chargebacks = 150 cases

150 divided by 10,000 = 1.5% chargeback ratio

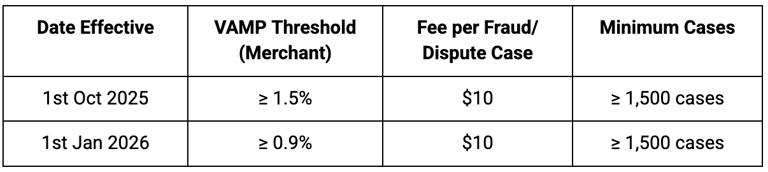

Key deadlines:

1st October 2025 - merchants must have a chargeback ratio of 1.5% or lower. If higher you will be fined $10 for every chargeback.

1st January 2026 - merchants must have a chargeback ratio of 0.9% or lower. If higher you will be fined $10 for every chargeback.

If you exceed these ratios, you will have a 3 month grace period where you won’t receive any fines to give you a chance to try to reduce your ratio. You receive a 3 month grace period for every 12 months you do not exceed this ratio.

Your payment provider needs to have less than a 0.5% chargeback ratio across the combined portfolio of businesses they provide payments to. If they exceed this, they get fined $4 for every chargeback (not just the ones that exceed the limit) and $8 per chargeback if their ratio exceeds 0.7%.

If they continually exceed this limit they will face fines, have to provide remediation plans to card networks and face pressure to offboard the worst offending merchants. If they don’t reduce their ratio, they risk losing their Visa license entirely.

Therefore, although the merchant threshold is 1.5% and then 0.9% from 2026, if your chargeback ratio is exceeding 0.5%, you may be at risk of having your account terminated. It is important to ask your payment provider what their acquirer’s ratio is to understand the risk to you. Also, ideally have a backup merchant account with another provider in place in case your account suddenly gets closed.

Why do Chargebacks happen and how to prevent them?

Fraud and fulfilment related issues cause ~70-80% of chargebacks. The rest usually come from operational mistakes (billing, refunds, cancellations). Here’s a typical breakdown:

1. Fraud / No Authorization (40–50%)

2. Merchandise/Service Not Received (20–30%)

3. Merchandise/Service Not as Described or Defective (10–15%)

4. Processing Errors (5–10%)

5. Canceled Recurring Transactions (3–5%)

6. Credit Not Processed / Refund Issues (3–5%)

Let’s explain each of these and list the best prevention measures.

1. Fraud / No Authorization (40–50%)

Cardholder claims they didn’t authorize the transaction. This is broken down into 2 categories:

Actual fraud - stolen card

Friendly fraud - I don’t recognize this transaction

Actual Fraud

Actual Fraud could be one person with a stolen card or it could be a group who have bought a million card numbers on the dark web and are trying to test which of them are real and they can buy things with.

How to prevent:

3D Secure - this is authentication which checks if the buyer is who they say they are whilst they are paying online. The benefit here is the fraud chargeback liability is shifted away from the merchant and on to the cardholder’s bank. So if every transaction went through 3D Secure you would have no fraud related chargebacks. You can force consumers to pay using 3D Secure for all transactions but you will experience a lower transaction approval rate (percentage of customers trying to pay vs. money arriving in your bank account). 3D Secure is mandatory in Europe for all high value transactions or transactions the cardholder’s bank thinks seem unusual and wants to confirm it is actually the cardholder. Therefore, it is well known in Europe. If you have high chargebacks the benefits forcing 3D Secure may outweigh the lower approval rate. If you’re experiencing high chargebacks from European consumers due to fraud you should be using this. 3D Secure is less common in the US and Canada and many cardholder’s banks do not support 3D Secure so forcing consumers to use it in these markets can lead to large declines. It is worth A/B testing turning on 3D Secure in each of these markets.

Apple Pay and Google Pay - Like with 3D Secure, a consumer authenticates themselves every time they pay with Apple Pay and Google Pay meaning the fraud related chargeback liability shifts away from the merchant and onto the cardholder’s bank. If you have customers paying via smartphones or tablets adding these is really worth it. After adding Apple and Google Pay, businesses typically see a ~20% uplift in the number of mobile and tablet customers who land on the checkout page and go on to make a payment. That’s a 20% increase in revenue overnight.

AVS and CVV checks - Address verification service (AVS) checks the address that the customer enters matches the address the cardholder’s bank has on file before approving the transaction. Visa and Mastercard estimate AVS checks reduce fraud by ~25%. Card verification value (CVV) checks the 3 digits found on a card are entered correctly before approving the transaction. Studies show CVV checks reduce fraud by up to 40%.

Card Testing Tool - Fraud tools can stop common patterns that fraudsters use to test cards e.g. blocking the same IP address (a device’s unique identifier) making thousands of transactions with every one declining.

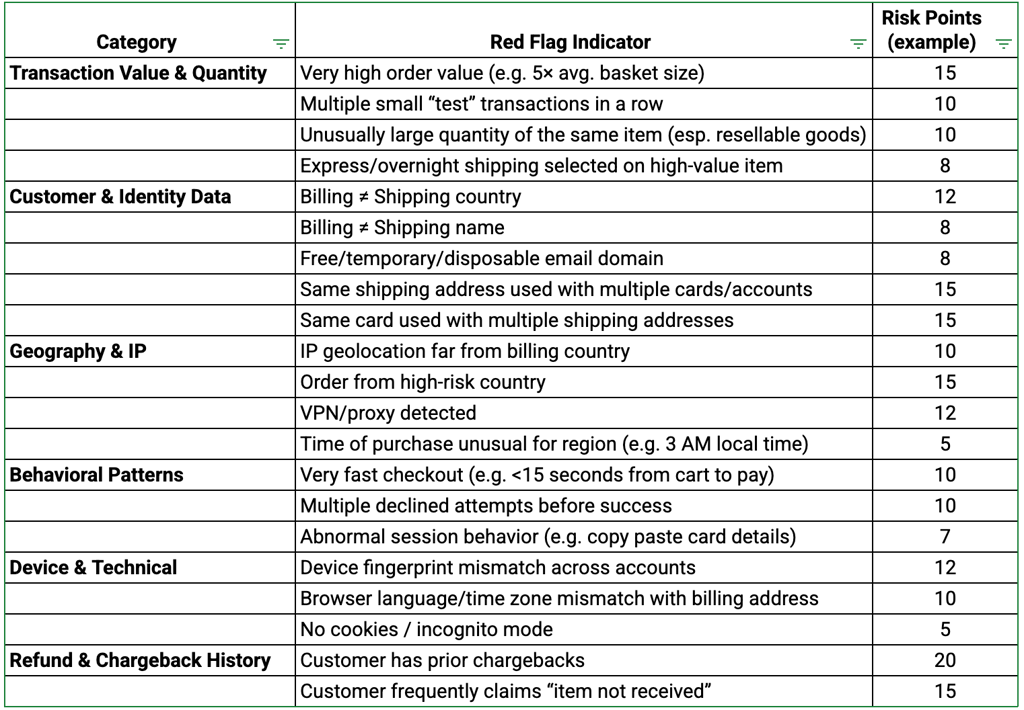

Fraud Tool - Use a tool that scores likely fraudulent risk factors to automatically decline or require approval for certain transactions e.g. the below table

Example Scoring Use

Safe order: Score < 20 → Auto-approve

Risky order: 20–40 → Manual review

High risk: > 40 → Auto-decline

Friendly Fraud

The customer made the purchase but later doesn’t recognize the charge on their statement.

How to prevent:

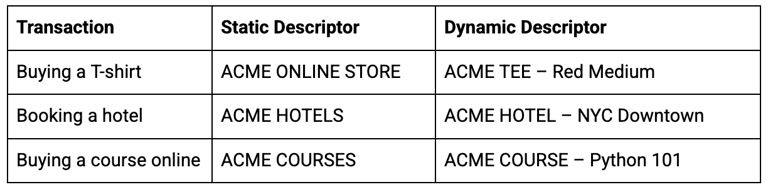

Dynamic Descriptors

A descriptor is the text that appears on a customer’s credit card or bank statement to identify a transaction. A static descriptor is the same for every transaction from that business. A dynamic descriptor can change per transaction to reflect the specific product, service, or merchant brand. Dynamic descriptors help customers recognize the charge, reducing confusion and lowering chargebacks. Some customers see a 30% reduction in friendly fraud chargebacks by implementing dynamic descriptors. It can also reduce customer support inquiries by 10%. Dynamic descriptors are automatic as they are sent through the API call when the transaction happens.

Example of Dynamic Descriptors

These are especially important for businesses who have many different products or services under their merchant account.

Keep the descriptor short and readable (usually 25–35 characters).

Include brand or product name.

Avoid cryptic codes or internal SKU numbers.

Ensure consistency between email receipts and statement descriptors.

Email confirmation

Send email confirmation with itemized receipts. Ensure the name on the billing descriptor is also on the email confirmation so they can find it after viewing their bank statement. Include a link to a page with a clear refund / return policy.

Make it easy and quick for customers to get a refund

If customers can’t easily get a refund through the email confirmation they received or on your website/ app, some will file a chargeback. Explain on your website how to make a refund.

1. Clear Refund / Return Policy

Visible link: Place it in the footer, checkout page, product pages, and confirmation emails.

Plain language: Avoid legal jargon. Example: “You can return any item within 30 days for a full refund.”

Step-by-step instructions: Explain exactly how to initiate a return or request a refund.

Best practice: Include eligibility criteria, timelines, and who pays for return shipping.

2. Simple Refund Request Process

Online form: Let customers submit refund requests directly on your site.

Minimal friction: Require only essential information (order number, item, reason).

Automated acknowledgment: Send an email confirming receipt of the refund request.

Best practice: Offer tracking or ticket numbers so the customer can monitor progress.

3. Fast Refund Turnaround

The faster the refund, the less likely a customer will dispute it via a chargeback.

Process refunds quickly (within 2–5 business days if possible).

Communicate clearly when the refund will appear on their statement.

4. Prominent Contact Information

Include phone, email, or chat support for questions about refunds.

Make customer service hours clear.

Offer multiple contact options to reduce frustration.

Tip: Having live chat during checkout can prevent disputes before they escalate.

5. Align Website Information With Billing Descriptor

Use the same brand name or dynamic descriptor on your site, receipts, and credit card statements.

Customers are less likely to file a chargeback if the statement matches the website/product they purchased.

6. Confirmation Emails & Receipts

Send immediate order confirmation and include:

Product/service purchased

Amount charged

Billing descriptor as it will appear on the statement

Refund instructionsFor subscriptions, include renewal reminders and easy cancellation links.

7. FAQ Section for Returns and Refunds

To reduce confusion and lowers disputes, preemptively answer common questions:

“How do I return an item?”

“When will I get my refund?”

“What if the product is defective?”

2. Merchandise/Service Not Received (20–30%)

Customer says goods/services never arrived. Common in shipping/delivery industries.

How to prevent:

Always use tracking numbers and require delivery confirmation/signature for high-value orders.

Communicate shipping delays proactively.

Provide digital delivery confirmation logs (IP address, device, timestamp).

Make customer service easy to reach before they go to their bank.

3. Merchandise/Service Not as Described or Defective (10–15%)

Item is broken, counterfeit, poor quality, or doesn’t match description.

How to prevent:

Provide accurate, detailed product descriptions & images.

Set clear refund/return policies.

Quality control on shipping & fulfilment.

Respond quickly to disputes before the customer escalates.

4. Processing Errors (5–10%)

Duplicate charge, wrong amount, expired authorization, incorrect currency.

How to prevent:

Check your payment provider integration is not causing duplicate charges.

Automate refunds for duplicate/failed attempts.

Use payment reconciliation tools to catch errors early.

Train staff on correct usage of the point of sale system.

5. Canceled Recurring Transactions (3–5%)

Customer cancels subscription but keeps getting billed.

How to prevent:

Provide a clear and simple cancellation option.

Send billing reminders before renewal.

Immediately stop billing after cancellation.

Send a confirmation email for cancellations.

6. Credit Not Processed / Refund Issues (3–5%)

Customer claims they returned an item/canceled service but refund wasn’t issued.

How to prevent:

Issue refunds quickly (within 2–5 business days).

Notify customers via email when the refund is processed.

Provide clear return policies and timelines.

Track refunds in case a customer disputes.

Chargeback tools

With all these preventative measures, chargebacks will be dramatically reduced. However, chargebacks will still come through. For certain types of chargebacks, there are tools which will enable you to intercept the chargeback before it officially becomes a chargeback.

When a cardholder reports a transaction as fraudulent with their bank (Reported Fraud mentioned above), there is a 24-48 hour window before that turns into a Reported Chargeback. In this period, you can automatically refund the customer.

This will still count as Reported Fraud (TC40) towards your chargeback ratio but will remove the Reported Chargeback (TC15) from your ratio.

The question is when should you refund and when should you fight the chargeback. Typically businesses refund about 40-60% of transactions and fight the other 40-60%. Here are some general rules on this:

1. Transaction Value Rules

Low value (<$20–$50) → Auto-refund.

Fighting costs more than the revenue.

Chargeback fee ($20–$100) is usually higher than the sale.

High value ($100+) → Challenge if evidence is strong.

Worth the effort to recover revenue.

2. Evidence Availability Rules

Refund Proof Exists → Accept liability.

If merchant already refunded but processor didn’t catch it, providing proof usually wins.

Delivery Confirmation (signature, tracking) → Challenge.

Digital Goods → Challenge only if login/IP/device usage can be proven.

No evidence (no tracking, no customer interaction logs) → Accept/refund.

3. Chargeback Reason Code Rules

Fraud (stolen card / true fraud)

Usually don’t fight unless 3D Secure, CVV/AVS match, or fraud screening passed.

Card networks rarely side with merchant in “unauthorized” claims.

Unrecognized Transaction (friendly fraud)

Challenge with descriptors, receipts, support logs, usage data.

Win rate here can be much higher.

Product/Service Not Received

Fight if you have tracking or delivery proof.

Product Unsatisfactory / Not as Described

Usually harder to win → may accept unless strong return/refund policy proof exists.

4. Customer History Rules

First-time customer, one-off fraud → Refund/accept.

Repeat customer, history of legitimate orders → Fight (likely friendly fraud).

Serial chargeback filer (abuser) → Flag/block, often refund rather than fight.

5. Processor / Risk Rules

High chargeback ratio merchants (close to Visa/MC thresholds):

May refund more aggressively just to keep ratios low.

Low chargeback merchants (well below thresholds):

More selective, may fight more cases to recover revenue.

Preventive measures are almost always more cost-effective: spending a few cents per transaction is cheaper than losing the transaction + paying $20 - $100 in chargeback fees + higher risk of monitoring programs.

Post-chargeback tools are useful as a safety net, not as a primary strategy. They protect your chargeback ratio and automate refunds, but they don’t save the sale.

“An ounce of prevention is worth a pound of cure.” Benjamin Franklin

Checklist

Calculate your chargeback ratio

Ask your payment provider what their chargeback ratio is across all their customers

Backup merchant account - if exceeding 0.5% chargeback ratio

Identify the main reasons why you are receiving chargebacks

Fraud / No Authorization

3D Secure - especially if you are selling to European cardholders

Apple and Google Pay - especially if you have lots of consumers paying via phone or tablet

AVS checks

CVV checks

Card Testing Tool

Fraud Tool

Dynamic Descriptors

Email Confirmation

Make it easy and quick for customers to get a refund

Clear Refund / Return Policy

Simple Refund Request Process With Confirmation Email

Fast Refund Turnaround (within 2–5 business days)

Prominent Contact Information on website

Align Website Information With Billing Descriptor

Confirmation Emails & Receipts

Provide accurate, detailed product descriptions & images

Set clear refund/return policies

Quality control on shipping & fulfilment

Respond quickly to disputes before the customer escalates

Check your payment provider integration is not causing duplicate charges.

Automate refunds for duplicate/failed attempts.

Use payment reconciliation tools to catch errors early.

Train staff on correct usage of the point of sale system.

Merchandise/Service Not Received

Always use tracking numbers and require delivery confirmation/signature for high-value orders.

Communicate shipping delays proactively.

Provide digital delivery confirmation logs (IP address, device, timestamp).

Make customer service easy to reach before they go to their bank.

Merchandise/Service Not as Described or Defective

Item is broken, counterfeit, poor quality, or doesn’t match description.

Provide accurate, detailed product descriptions & images.

Set clear refund/return policies.

Quality control on shipping & fulfilment.

Respond quickly to disputes before the customer escalates.

Processing Errors

Check your payment provider integration is not causing duplicate charges.

Automate refunds for duplicate/failed attempts.

Use payment reconciliation tools to catch errors early.

Train staff on correct usage of the point of sale system.

Canceled Recurring Transactions

Provide a clear and simple cancellation option.

Send billing reminders before renewal.

Immediately stop billing after cancellation.

Send a confirmation email for cancellations.

Credit / refund issues

Issue refunds quickly (within 2–5 business days).

Notify customers via email when the refund is processed.

Provide clear return policies and timelines.

Track refunds in case a customer disputes.

Chargeback tool

Payments Key

Payments Key offers a free chargeback assessment and reduction plan. Fewer chargebacks mean lower fees, reduced risk of service termination and access to more payment providers meaning better pricing and payment options.

Sign up below for a free chargeback assessment.